3 Key Points:

1. Medicare Bad Debt is experiencing many changes, including bad debt write-off timing and increased beneficiaries on Medicare Advantage Plans.

2. Extending the Medicare Bad Debt reporting timeline to 18 months potentially improves collection rates and minimizes write-offs.

3. Medicare Advantage plans necessitate rethinking bad debt calculations and anticipating a reduction in Medicare Bad Debt reimbursements.

The Medicare Bad Debt landscape is experiencing significant shifts, necessitating adaptations in how healthcare facilities manage their financial practices. With all the uncertainty, two key changes have emerged: the impact of credit bureau reporting on the timing of bad debt write-offs and the growing prevalence of Medicare Advantage plans. This article explores these changes and offers insights on how healthcare providers can navigate this evolving terrain effectively.

Revising Bad Debt Write-Off Timelines in the Era of Credit Bureau Reporting

In today’s healthcare finance environment, hospitals increasingly report to credit bureaus. Because of this practice, healthcare facilities need to strategically adjust the timing of transferring accounts to the Medicare Bad Debt route. Americollect’s recommendation is to extend this timeline for transferring accounts to Medicare Bad Debt to at least 18 months. This extension allows the effects of credit bureau reporting to fully materialize, potentially improving the collection rates and minimizing premature write-offs. Such a practice not only aligns with prudent financial management but also ensures compliance with evolving credit reporting standards.

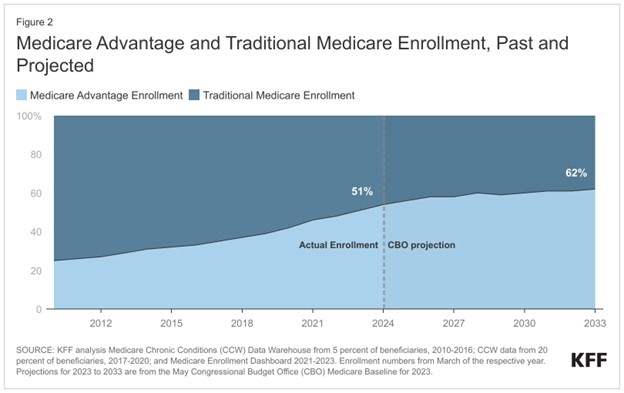

Medicare Advantage in 2023: Enrollment Surge and Its Implications

In mid-2023, the Kaiser Family Foundation (KFF) reported a significant milestone in Medicare coverage. Over half of Medicare beneficiaries (51%) are now enrolled in Medicare Advantage plans. This is going to force healthcare facilities to anticipate a reduction in Medicare Bad Debt reimbursements and rethink how they calculate bad debt.

Anticipating a Reduction in Medicare Bad Debt Reimbursements

The shift to Medicare Advantage plans signals a critical trend for healthcare providers as Medicare Bad Debt reimbursements are poised to decrease. The rise in Medicare Advantage plan enrollment necessitates a revised budgeting strategy, accounting for a reduced reimbursement landscape. Healthcare facilities must closely monitor the ratio of patients enrolled in Advantage plans versus traditional Medicare and adjust their financial forecasts accordingly.

Rethinking Bad Debt Calculation Methods

The last decade has seen more than 20% growth in Medicare beneficiaries opting for Advantage plans, which typically do not offer bad debt reimbursements. This trend prompts a need to reevaluate the existing methodologies used in claiming Medicare Bad Debt. While many of these new enrollees may not have previously contributed to bad debt, the sheer increase in their numbers warrants a thorough reassessment of bad debt calculation strategies.

KFF is predicting that this trend will continue upward, with over 60% of patients being on Medicare Advantage plans by 2033. In some instances, the recovery dollars collected by the collection agencies may be more than that in which you are reimbursed by Medicare. This doesn’t mean that theoretically you will lose Medicare reimbursements, instead, it might be better to delay the Medicare cost reporting until after the statute of limitations. This would allow the collection agency to continue to recover 2-3% year over year, effectively replacing the Medicare reimbursements. We recommend hospitals complete these calculations regularly vs relying on previously calculated assumptions and adapt their approaches to remain financially resilient in this changing landscape.

Conclusion

The evolving dynamics of Medicare, marked by the increased reporting to credit bureaus and the surge in Medicare Advantage plan enrollments, necessitate thoughtful and proactive adjustments in managing Medicare Bad Debt. Healthcare providers must stay abreast of these trends and adapt their financial strategies accordingly. By extending the timeline for bad debt write-offs and revising budgeting and calculation methods, healthcare facilities can navigate these changes effectively, ensuring financial stability and continued high-quality patient care. The first step should be looking for a collection agency that understands these changing dynamics – have you considered the Ridiculously Nice agency lately? If not, we would love to talk.

Ridiculously Nice Legal Disclaimer

The content provided in this communication (“Content”) is presented for educational and general reference purposes only. Americollect, Inc and/or AmeriEBO LLC either directly or indirectly through speakers, independent contractors, or employees (collectively referred to as “Americollect”) is providing this Content as a courtesy to be used for informational purposes only. The Contents are not intended to serve as legal or other advice. Americollect does not represent or warrant that the Content is accurate, complete, or current for any specific or particular purpose or application. This information is not intended to be a full and exhaustive explanation of the law in any area, nor should it be used to replace the advice of your own legal counsel. By using the Content in any way, whether or not authorized, the user assumes all risk and hereby releases Americollect from any liability associated with the Content.